Commercial fishing is a large part of the economy in Washington state. Various gear types and are used throughout Washington waters and are largely managed by the Department of Fish and Wildlife. Sustaining and vitalizing fish stocks into the future is important for the success of fishing fleets and the Washington economy.

Relevant Information

Fisheries Specific Information

For specific information about fisheries including salmon, Dungeness crab, Groundfish, Pink Shrimp, albacore, spot shrimp, sardine, anchovy, hagfish, and razon clams, read the full Sector Analysis Report on Commercial Fishing.

General Overview of the Commercial Fishing Sector

The Washington commercial fishing industry, inclusive of aquaculture production and

tribal fisheries, is one of the most productive and valuable in the U.S. According to the

annual NOAA Report, “Fisheries of the United States, 2012,” Washington ranked fourth

in landed pounds (420.1 million) in 2012, and fifth in value of landings ($302.0 million)

(NMFS 2013a). These figures represent four percent of the total landings and six percent

of the total value of all U.S. commercial fisheries.

The ports of Westport and Ilwaco/Chinook, both located within our study area, rank

among the most important commercial fishing ports in the country. Westport was ranked

13th by landed weight in 2012 (133 million pounds) and 16th by landed value ($59 million). Ilwaco/Chinook was ranked 30th by landed weight (29 million pounds) and 50th

by landed value ($22 million) (NMFS 2013a).

Washington ranked below California and Oregon in 2012 in commercial fishing landings

by weight, but above these states in landings by value (NMFS 2013a). Its most valuable harvested species included Dungeness crab ($59,485,000), albacore tuna ($28,440,000), and salmon (multiple species) ($28,398,000) (NMFS 2013b).

Commercial landings at ports within our study area (i.e., from Neah Bay to the mouth of

the Columbia River) account for a substantial share of landings statewide: 83 percent of

landings by weight and 63 percent of landings by value (DFW 2008). The value of

landings at ports in Grays Harbor County (including Aberdeen, Bay City, and Westport)

is the highest in the state ($19,262,100 in 2006), accounting for approximately 30 percent

of ex-vessel revenues statewide (DFW 2008).

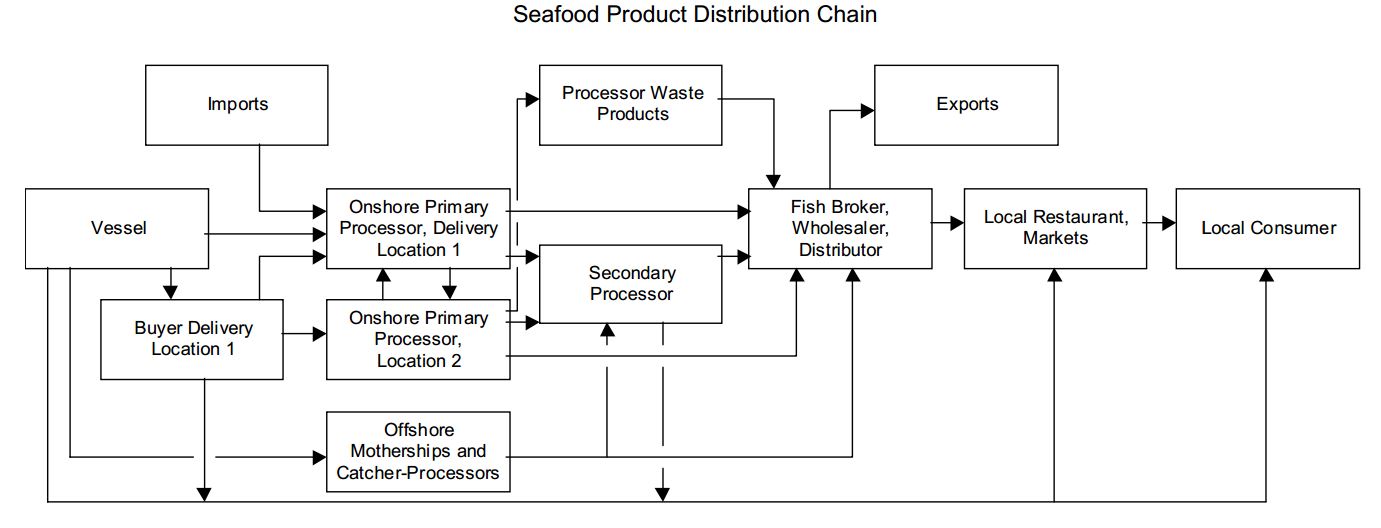

The diagram below shows the general flow of seafood from harvest to consumer. The majority of

the harvest landed in Washington is delivered to one of the many onshore processors

located within the state; in 2006, there were 104 seafood processing facilities based on

the Washington coast (TRG 2008). A share of the commercial Pacific whiting (aka

Pacific hake) catch, however, is processed at sea. In addition, onshore processing

capacity has seen some consolidation in recent years. As a result, the port at which the

harvest is landed does not necessarily realize the economic benefits of related processing

activity (DFW 2008).

According to a 2006 report published by the Pacific States Marine Fisheries Commission

(PSMFC), the majority of processing companies on the U.S. west coast depend upon

multiple species and markets. In addition, there has been a trend towards multi-species

dependency for high volume processors (PSMFC 2006). Factors that have affected the fish processing industry since the early 1990s include:

- Infrastructure issues related to whether water or byproduct use in the processing

process will overwhelm existing infrastructure; - A decline in wholesale prices for seafood;

- Major expansion of the onshore Pacific whiting fishery;

- Horizontal integration of processors and consolidation of processing plants in

fewer locations; - Vertical integration into distribution and harvesting operations;

- Return of small processors to offering specialty products in niche markets.

Source: PSMFC 2006

Source: PSMFC 2006

Economic Contribution of Commercial Fishing

Several recent studies, summarized below, provide insight into the regional economic

importance of the commercial fishing industry in Washington. Note that these studies are

generally focused on commercial fishing as a whole, and most do not differentiate

between activity within the study area (i.e., the outer coast) and outside the area (i.e., in

Puget Sound and the Strait of Juan de Fuca). Some include aquaculture, distant-waters

fisheries, and tribal fisheries, and thus are not representative of the portion of the industry

of interest to this effort. Comparison between these studies is not appropriate, as each

focuses on different components of Washington’s fishing industry.

DFW and The Research Group Reports

The 2008 DFW Report “Economic Analysis of the Non-Treaty Commercial and Recreational Fisheries in Washington State” responded to a request by then-Governor Christine Gregoire to “summarize the economic benefit that our commercial and recreational fisheries provide to the state” (DFW 2008). This study provides perhaps the most valuable existing information for our purposes, as it excludes aquaculture, tribal

fisheries, and distant water fisheries from the analysis. However, results are reported

statewide, and do not allow us to isolate that portion of the value of commercial fishing

activity attributable to harvests within the study area.

DFW (2008) relied in part upon information contained in The Research Group’s (TRG) 2008 report “Washington Commercial Fisheries Economic Value in 2006.” We report the values reported in TRG (2008) because they are presented in more detail (e.g., are broken down by species), but note they are slightly different from what was ultimately reported in DFW (2008).

TRG (2008) found that the commercial fishing industry was responsible for $148 million

in total personal income contributions, representing 3,530 jobs in Washington in 2006.

Although only representing a small fraction of total net earnings in Washington, this

income and these jobs are important to the economy of many individual communities on

the Washington coast and in Puget Sound. The net economic revenue generated by

commercial fishing was $38 million. The Dungeness fishery contributed the greatest

income, number of jobs, and net economic benefit of all fisheries (see below).

It is worth noting that the Seattle Marine Business Coalition took exception to the

findings of this report, and funded a study to develop what they believed to be the true

economic value of Washington’s commercial fisheries (Seattle Marine Business Coalition

2011). By including components of the fishery that they argue account for 28 percent of

Washington harvest values (i.e., tribal fisheries, distant-water fisheries, and aquaculture),

they report a total net economic value of Washington’s commercial fisheries as $3.9

billion (including recreational fisheries).

Community Attributes, Inc. Report

In 2013, Community Attributes, Inc. published a study for the Economic Development Council of Seattle and King County and the Workforce Development Council of Seattle-King County investigating the economic impacts of the sectors that comprise Washington’s maritime industry cluster, including Fishing and Seafood Processing (Community Attributes, Inc. 2013). Measures provided include direct impacts (gross business income and employment), indirect/induced impacts (employment and induced/indirect revenues/output), and wages. The results of the analysis are not directly applicable to the present analysis, as it includes tribal fishing, recreational fishing,

aquaculture/fish farming, and distant-waters fisheries. However, it could provide useful

context for ultimately understanding the overall contribution of coastal non-tribal

fisheries to the state’s commercial fishing industry as a whole.

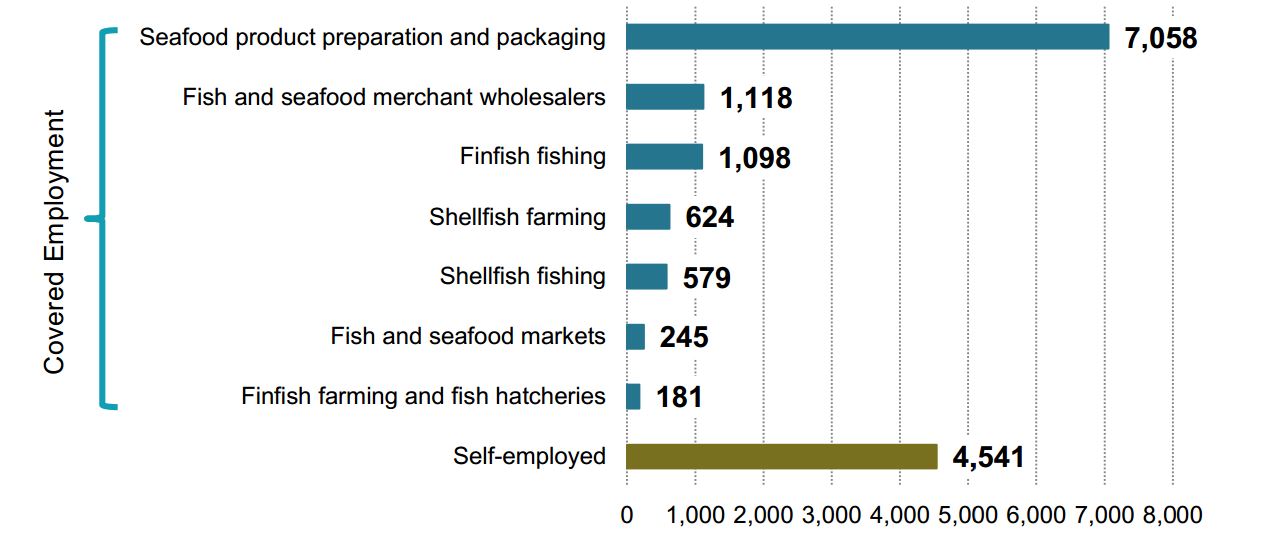

The analysis identified 720 establishments providing covered employment in the fishing

and seafood processing sector, and found a trend toward consolidation of businesses.

However, it also identified steady and even growing employment in the sector, with

approximately 11,000 jobs provided in 2011 (not including self-employed individuals

such as many fishermen (4,541 jobs)). The diagram below describes the number of jobs that are

supported by various sub-sectors of the Fishing and Seafood Processing sector. The

study calculated a total jobs multiplier for this sector as 3.0, meaning that for every job in

the sector, an additional two jobs are supported by fish and seafood processing activities.

Total wages generated by this sector were $1.1 billion. Gross business revenues were

estimated as $8.6 billion, and the sector contributed an estimated $135.7 million in tax

revenues to the state.

Fisheries of the United States

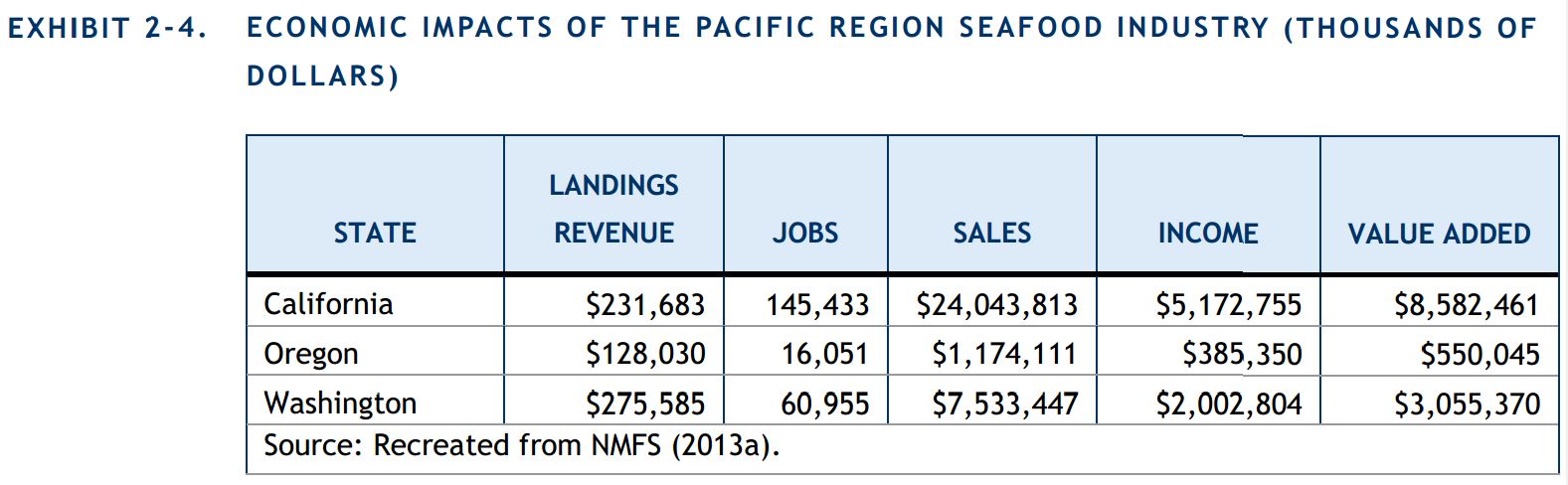

The 2013 NOAA report “Fisheries of the United States, 2012” reports that Washington’s

seafood industry was responsible for 60,955 jobs, $7.5 billion in sales impacts, and $2.0

billion in personal income, and contributed $3.0 billion in value added to the economy

(NMFS 2013a) (see below). These figures are not, however, strictly representative

of the segment of the fishing industry of interest to this report, as they include tribal

fisheries, aquaculture, and distant waters fisheries, and are inclusive of all state waters.

Expert Summaries: History, Trends, and Opportunities

The state of Washington has long been home to a vibrant and diverse fishing industry.

The Native American tribes in the region have been fishing for salmon, halibut and

shellfish for thousands of years, and European settlers have been fishing commercially in

the region since they arrived in the mid-1800s (Community Attributes, Inc. 2013).

List of Non-Tribal Fisheries Described in the Sector Analysis

| Commercial | Recreational |

|

|

Influences on Commercial Fishing

A number of events have substantially influenced the trajectories of the commercial and

recreational fisheries in Washington, including federal court decisions associated with

tribal treaty fishing rights. In United States vs. Washington (1974), Judge George Hugo

Boldt held that Washington’s native American treaty tribes reserved the right to take up

to 50 percent of the harvestable salmon in their respective usual and accustomed (U&A)

fishing grounds (384 F. Supp. 312 (W.D. Wash. 1974)). This ruling was also the basis

for their co-management of the fishery with the state. Twenty years later, in subsequent

cases under United States vs. Washington (1994), Judge Edward Rafeedie held that the

treaty right extended to finfish other than salmon, and shellfish, including oysters, clams,

and Dungeness crab (OCNMS IPC 2008). These rulings increased tribal involvement in

a number of commercial fisheries, and reduced the quantity of salmon available for

harvest by non-tribal fishery participants. The state/tribal management plans to

implement these decisions also include “special management areas,” which are closed to

non-tribal Dungeness crab fishing at certain times of the year, concentrating a lot of the

commercial fishing activity into the southern portion of the coast, particularly at the start

of the season (Personal comm. D. Beasley 2014, Personal comm. L. Thevik 2014,

Personal comm. K. Krueger 2014, Personal comm. M. Culver 2014).

Decline in the Salmon Resource

Another significantly influential event has been the decline in the salmon resource itself

due to factors such as loss of in-river habitat. This has resulted in a significant reduction in the number of salmon available for harvest by the tribal and non-tribal commercial and

recreational fisheries alike (Personal comm. M. Cedergreen 2014, Personal comm. L.

Thevik 2014, Personal comm. D. Beasley 2014, Personal comm. K. Krueger 2014).

Changes in the Fleet

These factors and others have substantially changed the characteristics of Washington’s

commercial and recreational fisheries. The sizable fleet that developed to target salmon

up until the 1970s now operates at a fraction of its former capacity (Personal comm. L.

Thevik 2014). Where non-tribal Dungeness crab commercial fishermen had historically

been able to rely upon participation in one fishery to sustain them financially, fishermen

today must participate in three to four fisheries in order to survive, which is more typical

of participants in fisheries that depend upon resource availability (e.g., salmon, albacore

tuna, sardines) (Personal comm. M. Culver 2014, Personal comm. D. Beasley 2014). The

lucrative Dungeness crab fishery that historically was dominated by coastal residents has

seen an influx of vessels from Oregon, Alaska, and Seattle (Personal comm. L. Thevik).

The commercial fishery participants are affected by competition from out-of-state, and other factors influencing wild fish populations, such as impacts on fish habitat (Personal comm. K.

Krueger).

Commercial Trawling Fleet

Another major change has been the near complete loss of Washington’s trawling fleet.

This loss was primarily due to the federal trawl buyback program, which bought out 92

permits along the West Coast, including five of Washington’s seven major trawlers

operating out of Bellingham, in 2005. This buyback was implemented through a loan

from the federal government, which the remaining trawlers are paying back through a

dedicated landing tax. This buyback was fully supported by the trawl industry via

referendum in recognition of the overcapacity of the fleet. The Pacific Fishery

Management Council (PFMC) worked with the trawl industry to develop a Strategic Plan

in 2000, which called for a fleet reduction of 50 percent; the buyback program was one of

the key steps to accomplishing this goal. While the full 50 percent target reduction was

not achieved, the buyback program reduced the total number permits to the current level

of 167.

Summary of Key Issues

| Issue | Concerns |

| Barriers to Entry an Success |

|

| Limitations in Use of Space |

|

| Ocean Acidification |

|

| Oil Industry Conflict |

|

| Overfished Species |

|

| Potential for Concentration of Ownership |

|

| Regulatory Uncertainty |

|

| Salmon Production and Survivability |

|

| Resource Sharing with Tribes |

|

Data Gaps for Commercial Fishing

The sector analysis report for non-tribal commercial fishing identified a number of gaps in the existing information that limited the development of a complete characterization of the sector. The most important data issues are described below.

- Employment data: Many fishermen are self-employed and thus are not captured

in traditional sources of employment statistics. This information is critical to

developing an accurate estimate of the economic impact of the industry. - Ecomonic impacts of ocean-based commercial fishing: Previous studies have

provided information on the economic impact of commercial fishing in

Washington. However, most analyses have included components of the industry

outside the scope of interest (e.g., aquaculture, tribal fisheries and distant waters

fisheries). We found very little information that helps us understand the economic

impact of the specific segments of the commercial fishing industry that are of

interest in developing the MSP for Washington’s outer coast. - Economic impacts of ocean-based recreational fishing: Previous studies have

provided information on the economic impact of marine recreational fishing in

Washington. However, most analyses are conducted on a statewide basis, and

cannot be isolated to our study area/counties of interest. We found very little

information specifically focused on the economic impacts of recreational fishing

along Washington’s outer coast. - Processor data: Previous studies have provided information on the economic impact of marine recreational fishing in Washington. However, most analyses are conducted on a statewide basis, and cannot be isolated to our study area/counties of interest. We found very little information specifically focused on the economic impacts of recreational fishing along Washington’s outer coast.

- Recreational Dungeness crab fishery: DFW does not track effort or catch in the

outer coast’s recreational Dungeness crab fishery. Note, however, that this

segment is a very small contributor to the overall recreational Dungeness crab

fishery, and thus might not be critical to the economic analysis.

Key Economic Questions

A number of existing studies have examined the economic impacts of the commercial and

recreational fishing industry on the Washington economy. However, there are a number

of questions not thoroughly addressed by previous research that should be considered in

the design of the forthcoming economic analysis. These questions are described briefly

below.

- Definition of the potentially affected industry: What is the most appropriate way

to define and bound the fishing industry potentially affected by decisions made in

the marine spatial planning process? Should the focus remain on non-tribal

fisheries whose catch comes from Washington’s outer coast, or should the scope

of the analysis be expanded to provide a more complete understanding of the

potentially affected industry and its economic reach? - Distant Waters Fisheries: To what extent do distant water fisheries (e.g.,

Washington-based vessels fishing in Alaska) generate revenues that are

brought into the Washington state economy? Should this activity be

included in the analysis? - Tribal Fisheries: What value are tribal fisheries bringing to the

Washington state economy? Should this activity be included in the

analysis? - Economic contribution of outer coastal fisheries: Nearly all available data on

economic impacts identified though the present process is reported at the state

level, and includes the aquaculture and/or tribal fishing industry. What economic

contributions are specifically made by the fisheries operating off Washington’s

outer coast? - Indirect services: How do/should we quantify services that are indirectly provided

by the fishing industry (e.g., the indirect benefits provided by a seafood

processing plant that purchases enough water from a public water supply system

to reduce the share of the system’s capital costs that must be borne by other

members of the community, or the indirect benefits to recreational boaters that

stem from dredging and other navigation improvement projects undertaken to

allow commercial fishing vessels to access fishing ports ). - Indirect recreational fishing value: Can/should we quantify the economic

contributions made to coastal communities when an individual’s planned fishing

trip results in the rest of his family visiting the coast, shopping, eating, and

contributing to the economy? - Community fabric/social value: How do/should we quantify or characterize the

non-monetary contributions made by members of the fishing industry to their

communities (e.g., through service on school boards, as volunteer firefighters,

etc.)

Fisheries Specific Information

For specific information about fisheries including salmon, Dungeness crab, Groundfish, Pink Shrimp, albacore, spot shrimp, sardine, anchovy, hagfish, and razon clams, read the full Sector Analysis Report on Commercial Fishing.